Tax coded as standardized and simplified Protocol for long-term stability

LANG(jezik): Global (en-us) / Local (sr-latn)

Short article: medium/tax-codex

CONTENT:

Preface | Progressive | TaxTypes | Simplification | Postface

Intro summary

- Implement progressive taxation (several tiers with rates: 0/10/20/../40 %)

- Have single model for all incomes (Income, CapitalGains same top marginal rate)

- Define VAT with a single flat rate 10, 15 or 20% (have child/family benefits for balance)

- Close all known loopholes (Trusts, Offshoring, make taxable loans backed by stocks)

- Optionally introduce 0.5% tax on assets over billion that goes to special development fund

- Simplify regulation and enable easier administration (global adjustable Protocol)

- Reduce monetary inflation and deficit and do tiers indexation every 5 years

- Limit public debt as well as maximum tax rates by constitutional law

Preface

Taxes are mostly boring and usually disliked (or even hated), but still are very important and relevant, both for individual person and for the broader community. One can not avoid them, not easily at least, so you should be educated about it and have an informed opinion. They also increase cooperativeness, a useful trait of human species.

Next to mention that taxes enable society to function at large, to manage shared resources and cover the costs. Some things can not be built and used individually, it is not practical nor efficient, because of scale and logistics. This includes public infrastructure, such as roads and city installations for water and electricity, that have natural monopolistic structure. In some cases also includes hospitals and schools assuming there are public ones. Additionally, there are costs of maintaining those facilities and institutions.

Civic society organizes itself as a country of citizens or a nation state. Always remember that the function of all Government Services is to serve the people and community, and never forget that politicians are your employees (servants) and not masters.

Next important issue is the level of taxes and their complexity, as well as how they are implemented and controlled/enforced. Firstly, it obviously can’t be either 0 nor 100%. Secondly, some consider it reasonable to have tax rates in the range between 10% and 50%. 10% or 1/10 (one tenth) was often a historic norm in the past. The 50% or 50/50 model is a common concept of fairness. Higher than half could be counterproductive as most people would be discouraged to work when the state takes too much or their earnings (motivation and incentive matters), and also it becomes prohibitive on economic growth. Even good intent, if not set properly, could lead to negative outcomes (the road to hell is paved with good intentions). Many socialist revolutions ended with economic collapse and failed spectacularly. Still, ethical considerations of redistributive taxation includes viewing it as morally virtuous to reduce extreme inequality and provide a safety net (Kant’s categorical imperative and justification / tax-justice).

In conclusion, up to 50% is considered by many conservative economists as Fair and socially optimal rate for balancing growth, equity, and incentives (even top marginal tax rates should not exceed 50%). Furthermore, individual responsibility of each citizen could mean having a moral duty to contribute to society and civilization.

More central stance would be to have majority of incomes taxed in ranges between 20% and 40% or 42% as an answer to the Ultimate Question of Tax (European OECD countries in 2025 have 42 avg. top marginal rate). Effective rate of around 20% could cover approximately 80% of people - in line with Pareto Principle 80/20 rule (Distribution of Taxes paid by Income Groups). Different countries, depending on culture and economic development, could have different limits, or Tiers so to say. These would be some general guidelines. For determining rates and tiers or band limits it should be looked into the public record of Income Statistics. It might take a few iterations to fine-tune them, just always start from first principles and keep critical thinking. It should always be kept in mind that the proportion of the budget with total public spending in a fiscal year and of GDP should not exceed a ratio of 30 to a maximum of 40%. During implementation of changes, it can be decided whether to aim for revenue neutrality to target slight increase, depending on previously mentioned ratio. Also, a phased pilot approach would be useful for enhancing the feasibility of a project.

Another issue with too high taxes is that people stop paying it and start actively working to avoid them - The Laffer Curve (optimal tax rate that maximizes state revenue). Some even think it could be as high as 70%, but that would be very unpopular and probably not socially acceptable, and also has some negative externalities with unintended consequences.

Also important to know why all of this was not already done, practical justification was that the rich would leave and another based on principle was that taking someone’s money is immoral. But if taxes are moderate and spent wisely, it would refute the criticisms. What remains is the real reason behind this, is that rich people have power and influence over the media, hire clever accountants who know how to find and use tax loopholes and are lobbying politicians.

Progressive model

In general, the tax model should be Progressive (how good is it), with a higher rate for higher income, but still having a maximum limit to be widely acceptable (having precise Highest and Lowest Bracket). It was designed more than 200 years ago and is already in effect world wide in many countries, especially in more developed economies. It represents an excellent way to smooth the tax cliff edge, that should be avoided at all costs, as it disincentivizes growth.

One could ask why such a model, a few reasons (why are fair):

-1. philosophical argument emphasising humanism/humanity (civilizational progress & taxation renaissance),

-2. better social cohesion and harmony based on adequate social contract, less strain on societal fabric,

-3. enables a more productive population, in other words, healthy and well educated and satisfied people are more fruitful, while those under constant stress lose creativity and fear taking even small risks,

-4. based on ‘ability to pay’ principle, meaning heaviest burden carried on the strongest shoulders (taxation equitable across income groups); but also ‘benefit’ principle - paid the most by those who benefit the most (more assets has a greater need of police, fire-department, etc)

-5. the marginal utility of money drops off the higher it gets, so a flat tax would be less fair because the burden is unequal.

Reducing inequality also reduces social division and tensions (less group friction and conflict) with more economic mobility due to real and effective equality of opportunity (where each person is then responsible for the outcome). The fact that one must look after themselves, doesn’t mean he can’t care about others, it is not mutually exclusive, just need the right balance. This would also lead to a happier population that could partially help with solving some of the pressing issues, like the housing crisis and low birth rates, although the latter is more of a cultural and psychological issue of modern parents. People have strong tendencies to compare themselves with their peers and current circumstances, and not with their predecessors or older generations nor how things were in the past (social comparison theory). Even if on average most people are objectively much better off than ever before in history, it wouldn’t matter, most will only care about what others have and do today, and digital social media only exacerbate the problem (‘get rich or die trying’). Partly because of that in today’s world having kids and also raising them into decent persons and productive members of society should be considered as one of important accomplishments in life and be commendable.

In a political-economic sense this would be a standard capitalist system with a moderate level of social democracy mixed with liberal democracy (social liberalism). History shows that this is most stable in the long run, and the least bad we know so far, while keeping as much individual freedom as possible. Somewhat similar to the Nordic model, mixture of a free market with less regulation. But with a strong welfare state, and labor market regulated by negotiations between labor unions and employer unions, where applicable. Another characteristic of this model is ‘Flexicurity’, relaxed hiring and firing regulations combined with strong social safety nets through government grants and social insurance.

Still, this model is not easily replicable in other countries (welfare hard to copy), due to different culture and internal solidarity, but also a fact that they are economically highly developed nation, have small population with relatively high income average. Nevertheless, one can be inspired by aspects of the nordic model and strive in that direction by implementing some elements to a certain level. One good example would be universal state-sponsored healthcare as market mechanisms here might not lead to efficiency, since sick people and in distress can not evaluate the quality of medical services, nor easily compare different hospitals. If compared to the US where it is more expensive but less effective, because of a largely private, for-profit system with a complex insurance structure leading to higher administrative costs and drug prices (denmark healthcare better with less money). America is one of few developed nations with declining life expectancy in recent years. Interesting hybrid model is the Swiss healthcare structure as a decentralized, universal system funded by a combination of taxes, mandatory private health insurance from non-profit insurers and out-of-pocket payments. Swiss have high-quality medical services and advanced technology.

When it comes to maternity leave, the US for example has a very bad record with only 3 months of leave and even that is not a universal benefit. Europe in this regard is much better with around 12 months of parental allowance. And it would be best to extend paid parental leave a few months more to 16, the last 4 divided equally between both parents for better bonding with the child. After that there could be subsidies for daycare or kindergarten in line with market prices until starting going to school.

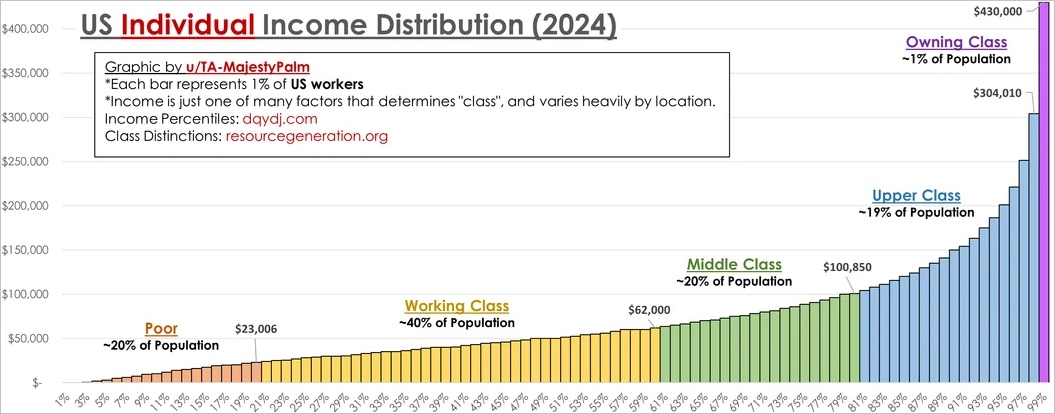

For estimating all potential effects, check the Income Distribution in a form of very useful visual graph below.

In the US bottom 20% of people earn up to 24 000 $ / year, while top 20% earners are above 100 K or even 120 000 $ annually as of 2025.

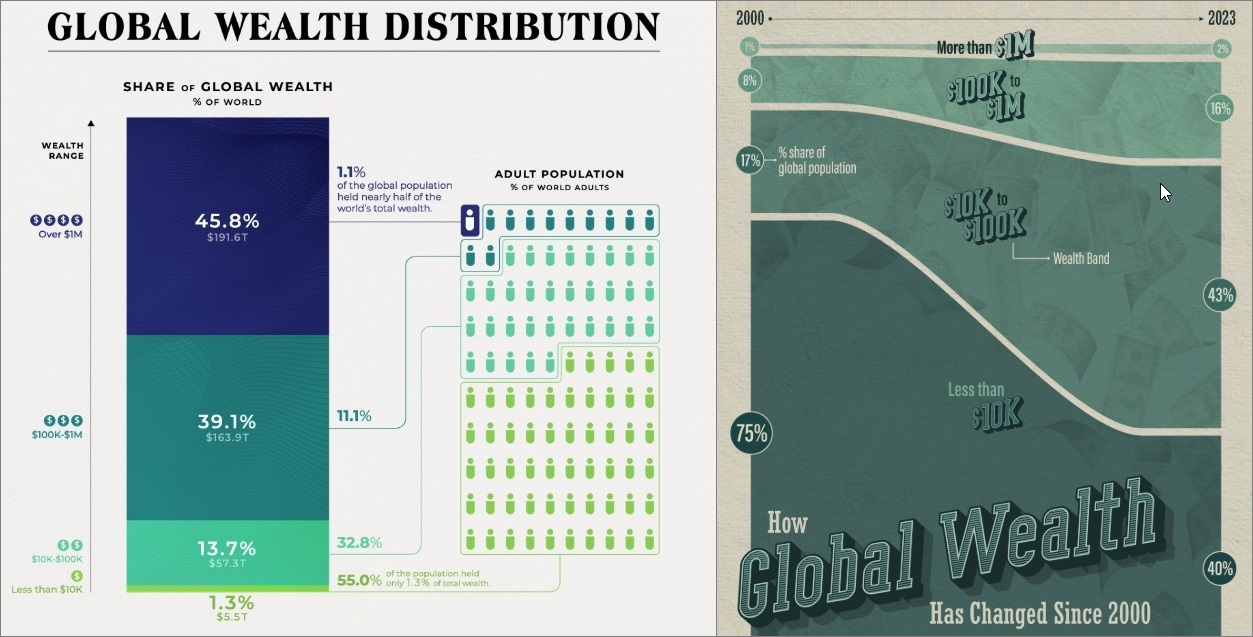

Distribution of Global Wealth - in 2021 and change 2000-2023:

(source: visualcap/wealth21 & visualcap/change20-23, also dataisbeautiful/wealth-range)

Tax types

Taxes could be grouped into 3 categories, based on either earning, buying or owning.

Tax types mostly in effect are: 1. Income, 2. Capital gains, 3. Corporate, 4. VAT, 5. Inheritance, 6. Wealth.

Focus will be on Personal Income tax and Capital Gains tax as they are direct and most important. Individual Income from labour but also from Dividends - US_Div (Ordinary or Qualified) and UK_Div with rates not quite the same as income rates, and it would be desirable to make all incomes equal (a singular tax model on income from any source). Bear in mind that for dividends that are paid to shareholders, the company already had to pay corporate tax on declared profit, but it is somewhat passive income so it can be considered acceptable. Fair amount of analysis was done on US and UK sample, since they have a long record of stable economy, and also developed tax system, but still have a lot of problems (TaxPolicyCenter: compare US internationally).

All tax related things should be Simple as possible in line with the KISS principle (elegance of simplistic design). Also there should be minimal difference between Income and Capital Tax, so that there is no distortion of either segment. This in practice could mean that tax tiers in both categories should be similar, while Social and Pension and Medical insurance should have max limit on mandatory part, with anything above to be optional. More precisely, basic health contributions should be the same for everyone and health fund to have 30% additional support from taxes. While pension contributions can be proportional, larger payment means larger pension, and with 2 pillars (second by choice over mandatory amount).

On the technical side, tax rules should be simple, and percentages to be round numbers with only a few incremental steps like +- 2% or 5%. There should exist several standardized tiers, for societies with different stages of development, that also could have specific culture and history.

(1) Income Tax (salary/wage and personal income)

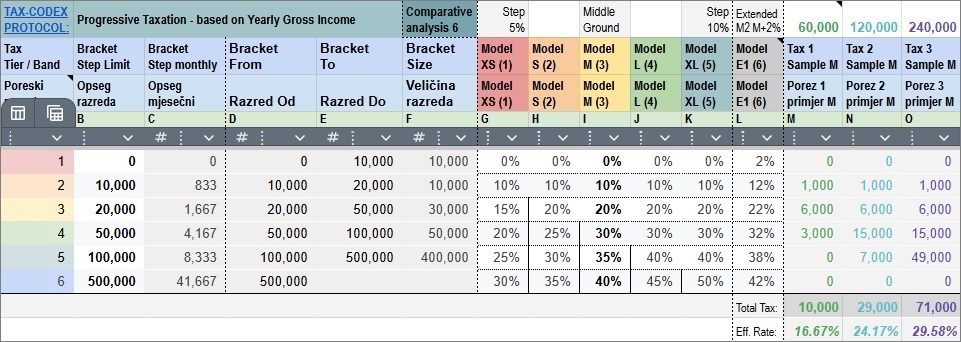

Brackets and increments example - to better understand concept (functional beauty in numerical math symmetry):

| № | From | To Amount | Step | Model XS | Model S | Model M | Model L | Model XL |

|---|---|---|---|---|---|---|---|---|

| 1 | 0 | 10 000 | 10 K | 0 % | 0 % | 0 % | 0 % | 0 % |

| 2 | 10 000 | 20 000 | 10 K | 10 % | 10 % | 10 % | 10 % | 10 % |

| 3 | 20 000 | 50 000 | 30 K | 15 % | 20 % | 20 % | 20 % | 20 % |

| 4 | 50 000 | 100 000 | 50 K | 20 % | 25 % | 30 % | 30 % | 30 % |

| 5 | 100 000 | 500 000 | 400 K | 25 % | 30 % | 35 % | 40 % | 40 % |

| 6 | 500 000 | no limit | - | 30 % | 35 % | 40 % | 45 % | 50 % |

-Tax Models: (X-Extra); S - Small, M - Medium, L - Large (M as the Golden Mean - politically most doable)

-First 10 K (around half of full time minimum pay) is tax free in all models.

-Represented as US yearly average $ value, should be scaled to each country based on their GDP per capita and/or median wage and specific currency.

-Another option is 8 brackets with 2 more rows: 200 000 i 1 000 000 with symmetry 1 2 5 (tab SCALE8 on sheet below), or to go with just 4 brackets 0/10/50/150 K (tab SCALE4).

-Due to inflation, caused by money devaluation, ranges From-To should be periodically updated and rounded, like every 5 years or so (do the Indexation). Good practice can be to choose new thresholds that are divisible by 12 months.

-It would be applicable only to residents, those with tax residency which usually means being in a country for more than half a year - 183 day rule. However, some like the USA impose taxes on all citizens, even those living abroad. This is something they can do because of their current, some would now say previous, dominance in the economic, military and political spheres.

Data examples and comparative analysis of models - Tax Codex data sheet - tab SCALE:

(can be copied on Google-Drive to do further examination and customization)

{Brackets can be divisible by 12 (12/24/48/96/480 K - SCALE-12M), to get rounded numbers for monthly thresholds}

* asymptotically approaching top marginal tax rate at highest income levels

* asymptotically approaching top marginal tax rate at highest income levels

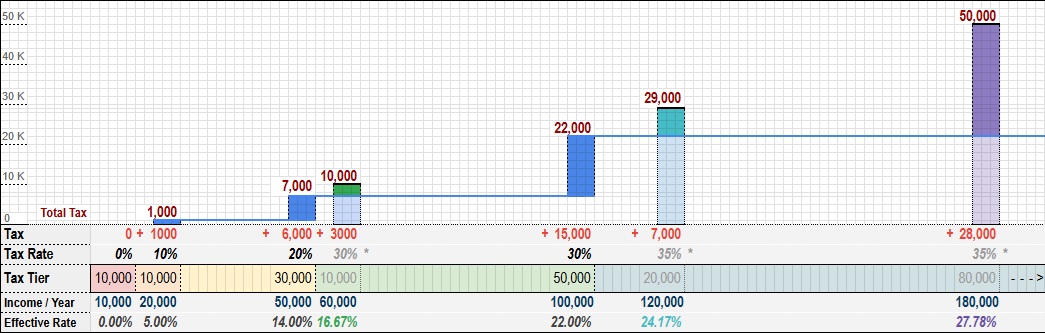

For example, with gross income of 30, 60, 120, 180 and 240 K total Yearly Tax and Effective Rate in model M are:

| Gross | Tax Calculation | Yearly Tax | Eff.rate | US.. / UK.. |

|---|---|---|---|---|

| 20 K | 10K * 0 + 10K * 0.1 | 1,000 | 5% | 5% / _7% |

| 30 K | 10K * 0 + 10K * 0.1 + 10K * 0.2 | 3,000 | 10% | 7% / 11% |

| 60 K | 10K * 0 + 10K * 0.1 + 30K * 0.2 + 10K * 0.30 | 10,000 | 16% | 12% / 19% |

| 120 K | 10K * 0 + 10K * 0.1 + 30K * 0.2 + 50K * 0.30 + 20K * 0.35 | 29,000 | 24% | 17% / 30% |

| 180 K | 10K * 0 + 10K * 0.1 + 30K * 0.2 + 50K * 0.30 + 80K * 0.35 | 50,000 | 28% | 20% / 35% |

| 240 K | 10K * 0 + 10K * 0.1 + 30K * 0.2 + 50K * 0.30 +140K* 0.35 | 71,000 | 30% | 22% / 37% |

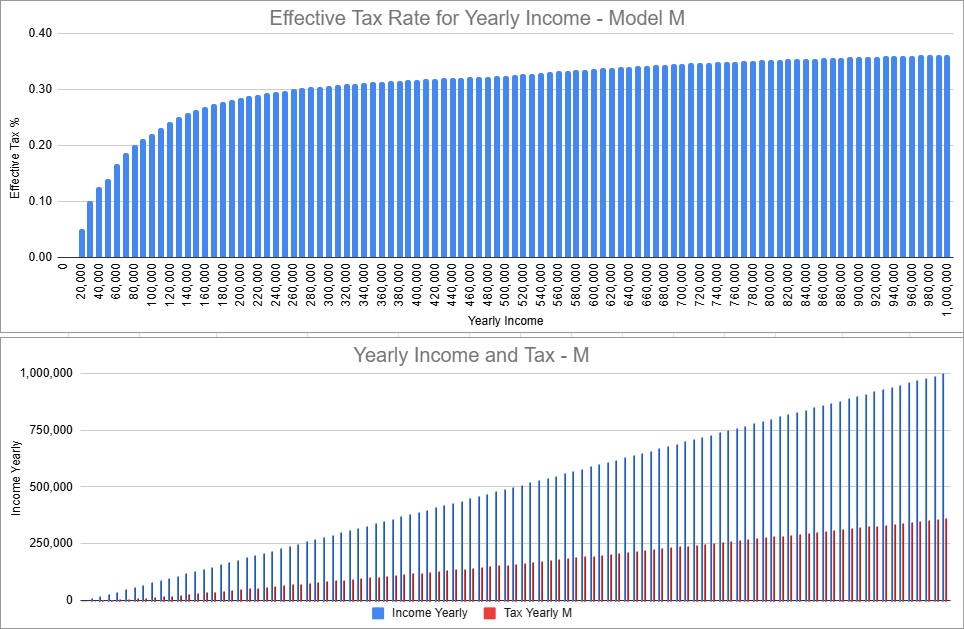

Tab CHART has sample of progressive chart, drawing with cells on digi graph paper:

One rule of thumb, based on common sense, would be to have less developed countries start with models that have lower taxes, and then every decade to aim for a higher model until it comes to optimal range. Changes should be gradual, step-by-step movement, to have smooth transition. For example in Denmark the top tier is 56%, which is above both median and upper line, but it still seems to work fine in their society, as they remain a country with high Happiness Score. So the remarkable thing is widespread acceptance of this very high burden and tax regime. Besides Denmark, several other countries could be taken into consideration for comparison including: Germany, Austria, Switzerland, Ireland, Norway, UAE, Singapore.

Currently the US has federal income tax with a top marginal rate at 37 %, while in the UK it goes to 45%. As we can see both countries already have progressive tax system where most are paying their fair share when it comes to Income tax, but Capital tax remains somewhat problematic. Tax expenditures (deductions, exemptions, and preferential tax rates) are a major driver of inequality, due to bad tax policy. Changes post 1980s in the US regarding capital gains and dividends were the largest contributor to the increase in the overall wealth imbalance. Hyper-Financialization, referring to the increased dominance and complexity of the financial sector in the economy, has been a significant trend over the past several decades, particularly since the 1980s. Many argue that such excessive Financialization of the entire economy, with control of the financial sector over everything else, is a major driver of rising income and wealth disparity. On top of this, high inflation and ever growing debt are just making the problem even worse, especially since the 2000s with tax breaks and cuts. Essentially, the stock market has become highly speculative with many bubbles, almost gambling alike. High inflation is forcing working people to invest almost all their savings and become traders, but they still lack the time and knowledge, and big market players are extra profiting by taking advantage of this information asymmetry. Even retirees are unknowingly funding those speculative waves, from which fund managers and banks are benefiting the most (small investors pay, banksters play - a Wall Street phrase).

(2) Capital gains - usually have lower rates then Income tax, in order to promote prudent long term investments and ventures. However this is a significant contributor to class stratification as it also works as passive income so much more scalable, in addition to the Cumulative feature of money that is not spent but reInvested. Currently in many jurisdictions long term (longer than 1 year) capital gains tax is mostly around 20% like in the US (bump-zone and cap-gains-25), while for example in France and UK goes up to 30% and 32%. Therefore it might be best to categorise capitals gain like any regular Income and apply the same or similar tax bracket on sum received from both. (YT: why rich don’t pay taxes and how avoid paying)

Relevant issue with gains tax is when a person never sold the shares and usually there were no dividends either, meaning no realised gains. Instead they just take large credits insured by stocks, so called ‘stock-as-collateral tax loophole’, also named ‘buy-borrow-die’ (YT: BBD - The Free Money Loophole and Mother of all loopholes) or ‘buy-borrow-hold’ strategy (BBD explained). Here the interest rate on loan is very low, more than market returns even, and significantly lower then tax rate. For such a situation, legislative consideration should be to have a tax event on realised gains when taking large credit that is secured by stocks and alike. Taxable events could be any time the asset is utilized to receive money from its value. Of course it would only apply over a certain threshold, maybe 1 million, and possible only on stocks as they are transparent and liquid enough (budgetlab/reforming borrowing; equitablegrowth/close borrow hole; taxnotes/no tax-free lunch).

There were even suggestions to go straight to taxing unrealized gains, but it would not be a good nor fair solution and would not work properly so we will disregard it. There is no issue when the founder of a multi million dollar company keeps ownership just to maintain control over it, while giving valuable service and products to the people. On the other hand when he sells it for money that acts as a wider option on all societal resources (change of potential usage), then it is justified to have that be a taxable event. Maybe some compromise could be to have a small tax like 0.4 or 0.5 % for value above 100 million and after 5th year since founding of company but to have it in-kind and in form of preferred stock (non-voting shares) and also put aside in a sovereign fund for at least 10 years.

So, simply closing the previously mentioned borrowing loophole would be more than enough. This could reduce the recently established unusual practice of stock buybacks for tax advantages. Since this borrowing closure is still a somewhat unusual proposition, regulation could initially be for a limited period, say 10 years. After that the results would be evaluated, before making it permanent or for a longer period in line with concept law expiration, explained below in more detail. Nevertheless keep a healthy dose of scepticism towards this suggestion, until proven as net positive.

When it comes to real estate, one main property where a person or family lives for more then 2 years ought Not to have Capital gains tax (Private Residence Relief) up to some reasonable limit (0.4M) and size (married couple single property with higher limit like 2.5x). Otherwise it would unnecessarily have bad stimulus on people not to move even when they change job to more distant location. In a high inflation environment, it’s crucial to differentiate between nominal gains (increasing price only) and real gains (increasing purchasing power). Taxes on nominal gains can sometimes distort investment decisions when they don’t reflect true wealth increases (tax rate to infinity). Reason more why we should get rid of inflation as much as possible, making nominal and real gains almost the same. But until then an argument can be made that the top marginal tax rate could be somewhat lower, especially for a longer period (5+ years) with higher inflation.

(3) Corporate tax could also have maybe 3 middle tiers to give support to smaller companies in order to promote healthy competition. Say 2% for small Sole Proprietorship (SP), 10% for smaller firms like startups for the first 2 or 4 years if they have revenue below some threshold like 1 million, and 20% for large corporations (anti-monopoly measure). At the moment, the US corporate tax rate is 21%, while the EU average is almost the same 21.5% but it ranges from 10% to 30%, depending on the specific country, UK has it at 25%. It should not be too high because when using profits to pay out dividends or even doing shares buyback which drives the stock price up, a taxable event would occur eventually. So with progressive taxes on dividend income, it would kinda be taxed twice, but for most people still below 50%, and it is passive income. On the other hand, employee salaries are expens so there is no double taxation there. Also many many large corporations are using different strategies such as foreign subsidiaries, and some loopholes to reduce the effective tax rate they pay. For example Google paid only 7% in 2023, with some paying even zero tax, while many paid on average 10 to 15%.

(4) VAT - Value Added Tax on sales (consumption tax) is also quite important. Most EU countries have it from 18% to 25%, the Swiss having it at around 9%, while the US does Not have any on federal level and instead has Sales tax only in some states at 7 or 8 %. Even the UAE, known for low taxes, has 5% VAT. The US deficit (1.8T) could be cut in half with new 10% Federal VAT that would bring about 1 trillion revenue. Remaining deficit could be resolved with 400 billion from increased revenue of capital gains, while the remaining 400 could be solved with spending cuts, 200 from military budget and 200 from other non constructive areas.

In general, many consider the optimal level for VAT to be between 10% and 20%, with 15% as a middle ground. And it should be paid only on collected receivable with option for monthly or quarterly accounting. Many countries have differential rates based on product category, a reduced one rate of 0 or 5% for basic food, some medicaments and baby equipment. And higher like 25% for luxury and exclusive goods that include special jewelry, expensive watches, high-end fashion, sports cars. For easier implementation and less distortion of market sectors and products, maybe it would be better to have only one rate, and fix the issues on other side with child benefits and maybe separate excise tax for tobacco, and optionally spirit alcohol as well. Besides, those who spend a lot, they probably have high income on which they pay higher tax rates so it is somewhat balanced there in the start. Finally, in order to eliminate any exemptions VAT should be paid also on financial services and banking industry (TaxResearch).

In the future this revenue might even enable some modest version of UBI - Universal Basic Income, or as some call it Freedom/Civic Dividend. Could be especially beneficial with all the technological progress and automatization including robotics and AI. But funding it to be only from regular taxes (‘trickle-up’ economy), not from debt nor money printing. Point is in using existing revenue and allocating it more directly and efficiently with lower administrative overhead. Another approach would be Friedman’s NIT - Negative Income Tax, to reduce complex social insurance schemes and unnecessary cost of bureaucracy while solving poverty. Furthermore, with NIT there is gradual transition of tax level as the ones income rises, instead of sharp benefits cut off that sometimes disincentivizes working.

Combined sum of Vat and Income tax should still in average stay under 50% for most people. To help with solving housing issues, the first house or apartment could be Vat tax-free up to a defined amount, and in addition to have loans subsidized for young couples buying their first home. Also, a significant part of Vat revenue should go Local communities.

(5) Inheritance tax, exists only in several countries where it is levied only above a certain threshold with different percentages. In some places they are referred to as Estate taxes.

One example for inheritance is Switzerland where it is not on federal level but cantonal, and applies only above 1 million CHF, and goes from 1 to 7%. On the other hand, the US (above 15 million, or 30 m. for married couple) and UK (above 325 K, or 1 mil. for couples) have a rate up to 40%. UK also has a 7-year Rule under which if inheritance is gifted 7 years prior to person death it is tax free. Personal stance here is that it would be appropriate to be up to 20% for values above 10 million $. When making a decision do note that not many countries have this type of tax, so it is not widely used. Having this tax too high could lead to frivolous and reckless behavior during life with wasteful spending on superficial things - bad version of extravagance. Note that many billionaires plan to leave each child only 10 million usd, in order to not spoil them with laziness. Also any exception, usually creates market distortion like for land of big farmers, which is then used as a loophole for the very rich buying a lot of farmland. So exceptions should be avoided, and make the rule moderate with a large enough threshold, say 1 million.

(6) Wealth tax is hard to enforce and could push people to move to other countries or states, even more so now with mobility of digital capital and wealth stored in cyberspace, and is not worth it (Super-rich leaving Norway or moving from California to Texas). Also, since it was previously accumulated, on which tax was already paid so there is no justification to tax it again every year, just like there is no excuse for taxing money savings with inflation every few months. Especially, since wealth or money will be used/spent in the future, at which point there it will again be probably taxed via VAT. Some countries, Denmark included, even have a small LVT - Land Value Tax (version of Georgism; book review Progress And Poverty by Henry George), from which income goes to local authorities. Similarly, some countries have small real estate tax on value of additional property above some threshold and size on primary residence, ranging from 0.1% to 1%. This revenue usually goes to the municipality (could be used for subsidisation housing loans for young people), and it could somewhat incentivize productive use of land and buildings by having it between 0.1% and 0.5%. Such properties are usually revalued every 2 or 5 years.

Even a small rate of 2% / year (as some are proposing) could end up being counterproductive, since it is not easy to implement nor to properly evaluate all wealth. Say, if a person has 20 million net worth of which 10 mil. is value of his company (privately held asset) where the rate of Return on Equity - ROE is around 8% so 800,000. Remember that there is 40% income tax and a person is left with 480,000. Then with 2% wealth tax being 200,000 the amount remaining would be 280,000 so total tax rate could come to 65% and effectively ROE comes down to just 2.8%. If we were to add Business tax of 15% that company already paid then effective tax becomes 70%. In some other cases with smaller profit like with 5% ROE, effective taxes would be over 80% of profit. That is why this is not a good model. Also, the wealthy are often competitive investors, most are not just sitting on their capital. And if their assets rise in value a lot then unrealised gains would be more sensical, or at least with less bad side effects. And always keep in mind the importance of property rights and personal freedom that the state sometimes infringe upon (Life, Liberty, and Property - fundamental natural rights by philosopher John Locke used in US Declaration of Independence).

Some would levy wealth tax, also known as capital or equity tax, on billionaires, a billion+ net worth individuals, and in the US among 340 million people there are less than 1000 such ultra-wealthy individuals (Forbes richest list and real-time), but I remain sceptical how effective it would be. Another proposal was for a one time tax, which might not have prolonged side effects, but still it could have negative results overall. However, here is one peculiar idea, to tax past the first billion at a rate 1 percent once every two years (1% / 2y, annually rate 0.5%) and put those revenues into a special development fund. The fund in question would be for scientific and technological research, that could include investments in renewable energy (most important resource of future) like better solar panels (perovskite), efficient battery storage (sodium-ion and solid state, green hydrogen production (electrolysis), nuclear fusion (small modular reactors - tokamak).

This should be more than tolerable and would help with extreme wealth concentration. In addition, it could also help increase ownership dispersion of unicorn companies as most of multi-billion wealth is in shares of a companies (allow for in-kind payment to sovereign wealth fund possibly). The condition could be that there is no tax for the first 10 years after establishment if the company has not made a profit in at least 2 years. In addition, an lower rate could optionally be set at a lower threshold, for example 0.1% for over 50 million, while 0.5% remains for over a billion. Effectively, the largest and highest quality potential and productive assets are real estate (land, houses, buildings, etc.) and equities of companies. These 2 types practically make up almost 80% of the important assets that these 2 taxes would cover, but only in an extremely high concentration, and with small percentages. This could collectively provide incentives for extremely large assets to be used productively and profitably and not just sit as dead or insufficiently profitable capital. All of this would force a certain minimum return on large capital.

(7) Inflationary tax i.e. direct money creation could be used to reduce indebtedness and thereby the unnecessary high cost of interest on it. When the debt is eliminated or reduced to a sufficient level, then the rate can be reduced or the inflow can be redirected to the development fund.

Table types and models

| № - Code | Tax type | Threshold | Model 1 S | Model 2 M | Model 3 L | Note |

|---|---|---|---|---|---|---|

| 1 - INMC | Income | 6 tiers | 0/…/35 % | 0/…/40 % | 0/…/45 % | select and apply |

| 2 - CPTL | Capital gains | same or : | 0/10/25 % | 0/15/30 % | 0/15/35 % | similar tiers |

| 3 - CRPR | Corporate | 0/100K/1M | 0/10/10 % | 2/10/15 % | 5/10/20 % | elaborate |

| 4 - VAT | Vat | - | 10 % | 15 % | 20 % | diff.M2: 5/15/25% |

| 5 - INHR | Inheritance | 1/10/100 M | 0/10/20 % | 5/15/25 % | 10/20/30 % | to consider |

| 6 - WLTH | Wealth | property | >0.5M 0.1 % | 0.2 % | 0.4 % | to Local 0.1-0.5% |

| ******** 7 - INFL | Inflation tax | cash savings | 1% | 1.5% | 2% | money supply |

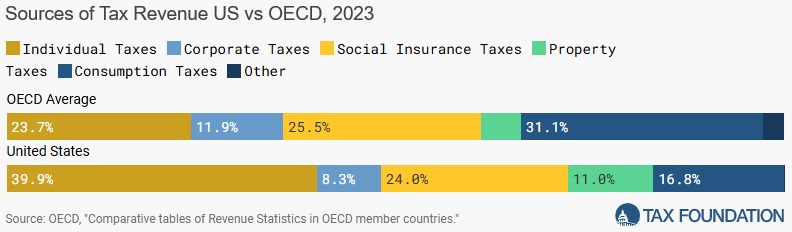

Revenue sources based on tax type US vs OECD-Organiz._Econ. CoOperation & Development (TaxFoundation):

Taxation Simplification

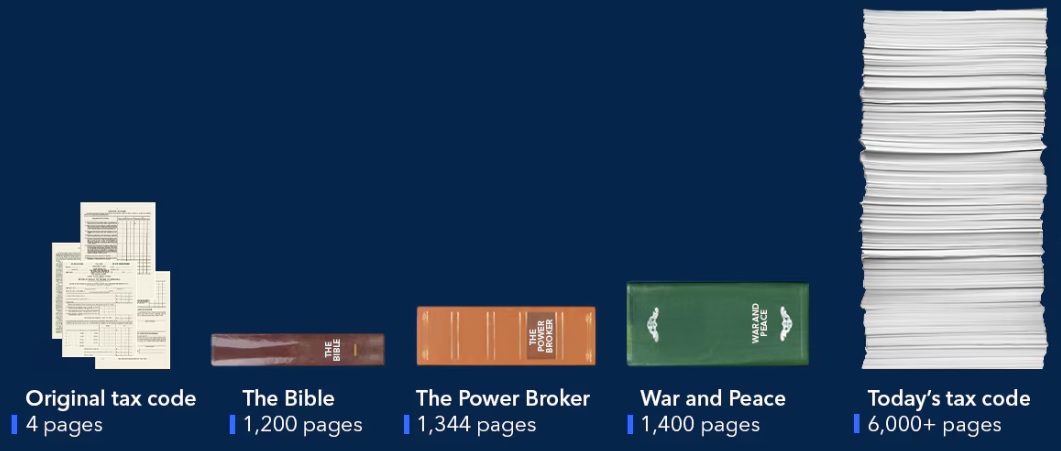

A simpler tax code means simplification of taxes for everyone. Redact 6000 pages tax code to less then 100 where besides main models additionally keeping only an effective set of deductions, with basic short edition in 10 pages (less chance for a bug aka hole). Also, one good technical facilitation would be to use digitalization and advanced software by tax authorities to create and prepare pre-filled tax forms ready for submission with just email confirmation.

Emphasys should be on sustainability and stability, with balanced budget and long-term planning. That is why this would be considered as a Protocol with standardized rules and the generalization of the tax system (Engineering of taxation - a technical approach to solving complex tax problems). This would make filling digitized reports for the Tax Authority much easier (using API), both for firms and also for accountants. And paying taxes could be made automatically using pre-programmed payments standing orders (tax pay on autopilot). Also as money is becoming ever more digital, payouts from the budget with clear rules could be pre-programmed, hence reducing bureaucracy and inefficiency. Total budget plan could be based on previous year revenue, with some buffer for differences, so no need for imprecise projection. This would eliminate overly optimistic predictions about future growth used as an excuse for excess spending. With all that, even ERP systems could then become more Protocol-like (work in progress) and would have most settings parameterized. This would enable them to be easily configured for any country or any tax type. Excellent combination of Smart Money, Smart Taxes and Smart Business.

Still in the long term, all countries should aim towards more unified ranges, as human values should be universal. It could also make the world more stable, with less issues for tax avoidance using offshore zones and tax havens, also called secrecy jurisdiction. That practice needs to become illegitimate in order to be reduced. If taxes are not too high, then tax avoidance should not be considered an achievement or admirable. Another issue would be fully illegal tax evasion. In the meantime more global coordination would be needed (global minimum tax for businesses of at least 15%), and special inspection of trust funds. Trusts have high legal expenses (lawyer and paperworks) and practically are only available to persons with very high net worth, privilege of the rich or unfair advantage (how trusts avoid taxes). For closing the loopholes it would be best to call upon experts in accounting, finance, and lawyers that have actually worked on creating these schemes, and use their experience to fix it permanently. Also to have a reward if someone finds a hole that could be exploited, similar to how IT systems often has prizes for white hat ethical hackers that discover bugs or security issues and help with patching it (tax holes bounty).

Several last decades we have witnessed higher inflation. Since 1980 total rise in average prices is around 4 times (with average yearly inflation ~3%), while M2 money supply rose 14x (averaging to ~6.2% per year). Difference is due to several factors: technology driven productivity pulling the prices down, dollar a world reserve currency and US exporting inflation, excess money going into properties and stock so average inflation is lower as assets higher. M2 is not perfect proxy for all the money supply, including debt which create money, but it is good enough approximation. It is obvious why discretionary approach to such a sensitive thing is dangerous as it becomes manipulated. So instead of letting this high inflation having very bad effects, it could be better to place strong constraints on money creation.

Thing to have in mind, for future sake, is that if we ever reform the monetary systems to permanently low money inflation (like k-percent rule, say 2%), then currency itself would not rapidly lose value as today. And the treasury could have a reserve fund for crisis situations to still have some monetary influence if needed. In such an environment monetary premium of non productive assets like real estate would reduce greatly, hence capital gain taxes on those would not be significant, instead income from labour and direct capital like dividends, would be more important, as well as revenue from Vat. This would be good as it would make taxation less complicated and easier to implement.

Postface

Progressive taxation is key pillar of modern societies. Tax marginal rate limits (e.g. min 10%, max 45%) should be set with constitutional law so that it needs a supermajority (2/3) of parliament for change - using existing legal framework. While in that range different models could be changed with simple majority but this should not become regular practices, only if not absolutely needed. Any change should be publicly discussed and debated, also planned in advance with any effects calculated into a model, so that everybody is prepared and knows what to expect ahead of time. Similar to how Linux, open source operating system, has regular yearly version updates in the same month, an ultimate predictability. Of course, compare Gini coefficient (measure of wealth inequality) before and after reform or any changes.

Another interesting idea is to have this Law, but also other laws and regulation to be on Github, an excellent collaboration platform, that has great visibility, transparent procedure for update, and detailed history of changes - audit info and track record. This was tried in Washington DC with authoritative digital source laws, sort of like The Legal Repository (Git for policymaking and Version control for law). Of course, a solicitor or legal professional could consult IT experts or tech-savvy individuals for advice using such a tool. To add that such systems need to have data backup with local copies regularly on daily bases to 2 separate safe locations (high redundancy). On top of that to have paper copies as well in a secure archive (document vault), with number and version in the header, where each sheet would be one segment so that only those with changes would need replacement.

In addition, laws themself could have conditional expiration (sunset clause or provision), say 50 years (with exception to constitutional laws), after which they should be reviewed, and discarded if obsolete or renewed(confirmed) with optional amendments. This would help to keep regulation smaller and effective, and at the same time gives each generation a direct chance to express their stance and opinion about matters in question.

Lastly, government spending is important as well. The idea that have been spreading lately how fiscal responsibility is absolutely irrelevant is complete nonsense, MMT included. Real economy, as well as resources and production, have natural limits and so does the state budget. Also taxes need to be public and have broad support from citizens. High monetary inflation is the ultimate example of the too big to fail concept, hence politicians can’t be allowed unconstrained access to such powerful and dangerous tool. Absolute power corrupts absolutely, as proven many times by history. Last few decades we all have witnessed ever growing deficits, with debt ballooning (now often over 100% of GDP) and money printing overuse. Even with all that, there are smaller investments in public infrastructure, and growing wealth gaps over the past few decades. This is due to lower taxes, and higher inflation that acts as a regressive tax as wages are sticky and don’t rise as much as prices while fiat currency has no constraints. It is not good when money printing, either direct or indirect, is used significantly to finance regular government operations. Much better and safer way is to have focus on taxes, because they have more checks and breaks with natural limits, can’t surpass 100%, and are more democratic/decentralized, as opposed to centralised and obscure money creating that is also susceptible to manipulation.

Any credit should have such incentives to be used for new investment, and less on everyday expenditures (reduce the Consumerism and its bad effects; and how Creditism replaced Capitalism / are we living in it?). This statement holds equally true for individuals, companies, and countries. Denmark again, even here, stands as a positive example with very little or no deficit accrual, so Danes live better with less, compared to US citizens. Switzerland is another role model, with a decentralized but efficient government that has historically maintained a low deficit. They have a “debt brake”, a constitutional rule that limits government spending to the expected revenue over the course of a normal economic cycle. This rule helps to ensure fiscal stability and prevent excessive debt accumulation. Country constantly paying interest for ever growing debt on money it controls is unnecessary and just bad practice. Overall, at least about 10% of the budget should be allocated for development and investments including new infrastructure projects, not all going to basic consumption. What is needed is accountability in public spending with conventional budget discipline and traditional view of fiscal policy. There are interesting articles and analysis regarding the subject from 2 organisation, one being IFS - Institute for Fiscal Studies and other IEA - Institute of Economic Affairs (Tax and Fiscal Policy) which is more right-wing but one can still filter some useful constructs from there or be better informed on different spectrum of opinions.

As always, one should approach the issues with caution, as public companies over a long time are prone to mismanagement. So either to have multiple strong checks and balances that are independent and separated with mechanisms to ensure they stay as such. Or to have more private sector and contractors, while keeping transparency in public procurement with fair tenders, equal for all participants. Finding and maintaining a delicate balance in such dynamics requires dedication and constant work, as optimal equilibrium is often fragile. Otherwise, it can easily turn into populism in the political domain and crony capitalism on the economic side. If there is too much corruption and misconduct, and if money from the budget is wasted on unproductive things or misallocated, then people would not see the point in paying their “fair share” to society, and would lose trust in institutions.

I would be very cautious with advocating these changes immediately in very corrupt places, first people would need to curtail it to a bearable level, and only then implement tax changes. Start first with the top income tier as they usually have political connections in those locations. Otherwise it would just be misused. Also too much expenditure on the military is not seen as great utility. While if the system is efficient, where for example all children have good schools with more egalitarian chance for success, then not many would oppose a slightly higher taxes. Still, not too high, so that most would pay it willingly, as a reasonable thing to do. They would know it has a good purpose with noble cause, and will benefit them as well (most people have kids, and they go to school). Young generations deserve a level playing field, especially in education. Lastely, one positive way to look at it is that high earners and those with large income are successful in their profession and are also biggest benefactor to society, so philanthropy by default or phrasing it as taxative altruism (legacy through taxation - public display of list with largest contributors). Person could be happy for paying more taxes even with a higher rate, as it means he/she is earning more.

Most ideas and concepts laid previously are not new, just gathered together into compact and comprehensive models, with few new features for modern age. They are collected from history and by examining the best practices from around the world and merged into this policy-oriented manifesto.

Finally, how could these changes be made? Learn as much about the problem and about potential solutions. Everybody can send notes to their political leaders asking them to incorporate this agenda as an active issue that should be worked on. Then in future elections vote for the party or more specifically for individual candidates that align the most with these proposals and support the objectives. This would not be an easy task and could take a longer time, but one should start now and think about future generations. In the end, the majority can vote for what is in their best interest (although often vote against), but also must look after the entire population and to keep the economic wheel working smoothly, have rational approach, although most humans are more rationalizing than fully rational beings). The broader consensus is reached for the selected model, the better. Finding a compromise (sweet spot) amid diverse political ideologies and opposing views requires the majority of people to be pragmatic and to stay optimistic realists. In the end, implementation of this protocol and initiatives for tax reform (one being Tax Policy Associates Think Tank) depends mostly on civic awareness of people and consequently political will of elected representatives, legislators and government officials. Would be for the best if all political candidates had to pass a test of basic understanding of the taxation system. Also one can find many intriguing reports and articles at TheTaxAdvisor as well as with Tax-consulting thinkers.

APPENDIX - only on LOCALized post

Leave a message: IP comment Form (comments list - firstByAI and sheet for review)

List of all referenced Links

Infopedia blog subscription Form - Newsletter

Supported by codis.tech